York City - Financial Accounts: 2022 And Onwards

All the information below is sourced from public records and press statements. Full sets of accounts are lodged at Companies House and should be available to anyone to download from their web site. This page deals with City's accounts from 2022 (the end of the Jason McGill era). See City's Accounts - The First 100 Years for all earlier years. Note, given the size of City’s business:

Transition (McGill - Henderson - Uggla)

It won't be for 3 seasons that the new regime, post Jason McGill, are in full control of the finances:

2022: The Reality - Income

In the matchday programme (December 3, 2022, v Wrexham), New CEO Alastair Smith quoted 2,219 season tickets “sold” and broke down City’s take. For a £299 season ticket, City pay VAT (nearly £50) and £23 (£1 per game to SMC) meaning City’s cut is £226.17. Match day admission ticket income works in the same way.

He went onto say that City’s stated 2,219 season tickets ”sold” figure includes volunteers, free carer tickets and those sold as part of hospitality packages. The split between full price adult ticket, concessions and junior means that each season ticket sold nets City an average of just £137.22 per season ticket, or £304,491,20 for the 2,219 “sold”. The budget had assumed £211.88 (not £137.22), way short of the actual.

Equally, the average proceed from a walk up match ticket is £10.21 (against a budgeted figure of £15.04), in both cases (season and match day tickets), City’s average take is just less than half an adult ticket’s face value.

All in all, average ticket proceeds are coming in well under the budgeted figure which means a shortfall. In income in December, Alastair Smith noted the budget was “already adverse by £200,000 and will only get worse over the remaining matches” of the season.

Maybe, part of the shortfall can be clawed back up by the fact that the budget was based on 2,000 season ticket sales, itself a number believed to be higher than in recent seasons. A little more assuming the budgeted 4,500 average attendance is exceeded.

2022: The Reality - Expenditure

For 2022/3, expect the total wage bill (all playing and non playing staff) to exceed total revenue from ticket sales.

Remember, on top of a someone’s base wage, there are other costs, commonly including employers’ national insurance and pension contributions, and in the case of players, presumably there is a bill for medical expenses / insurance.

It is believed that City’s player wage bill reached £2.75m in 2000/1 in the latter dark days of the Craig excesses. Today, it is unknown what the playing budget is, but from the limited account information that has been provided over the years, it is probably under £1m.

Equally, recent published figures might suggest total club turnover is less than half of that 2000/1 player wage bill.

Whatever, and in common with most clubs, the player wage bill will be a significant part of the total expenditure, indeed, 50% - 75% is not uncommon, still some Championship clubs spend twice their match day income on player wages.

For City, after wages, Alastair Smith expects a £190,000 spend on stewards, medical staff and police during this (2022/3) season.

Another 6 figure cost will be the enhanced facility fee (rent) payable for the extended 8,000 LNER capacity. The costs go on. Another big bill will be travel, Alastair Smith estimates that each overnight away trip costs City about £4,000. Barnet spend £5,000 on a trip up north. Other significant costs will be the cost of maintaining the training ground and vehicles that the club needs to function. Somewhere in the debit column might well be a hefty bill for food for the players at the training ground and on match days. Just like our own personal finances, City will be regularly hit by unexpected bills.

At the start of 2023, City loaned Shaq Forde and Ollie Tanner, social media posts suggested that City are contributing £600 per week of their wages. It is highly likely that City’s costs will also include providing accommodation for them in York for 5 months. Likewise, it is unclear what costs City might contribute to their contracted players in terms of housing accommodation and / or travel expenses. I recently heard Richard Brodie saying when he signed one of his City contracts that City bought him a train season ticket from Newcastle to York. Image the cost of that today.

It is down to commercial functions, advertising, sponsorship, merchandise, hospitality, concession sales and other incomes to plug the gap.

Failure to plug the gap between income and expenditure can result in a reduced budget at best. The worst doesn't bear thinking about.

9 Months In - The Reality

In April 2023, Alastair Smith noted.

The legacy debt is a contingent liability to Jason, it’s the remainder of the sum he wasn’t repaid on the sale on Bootham Crescent, after he had written off some of the interest. It is only payable as a percentage of exceptional income over the next 4 years, at which point any remainder is written off. Exceptional income is classed as large transfer fees, income from cup runs, crowds over a certain size, Jason has said that he wouldn’t ask for the money if it was going to leave the club in a financial problem.

There are commercial opportunities at the LNER, in benchmarking commercial income YCFC is way off the standard expected of a club our size who rent their stadium. The club is entitled to 4 free nights a month to use the facilities, to date the club has held a couple of TV games, a fans forum, and a quiz, we need to do much better, but it needs time. Steve Ovenden has offered to raise £50K by putting events on at the LNER, if anybody is able to assist with their time, ideas, and supporting the events Steve arranges that would be really appreciated.

We have 6 hospitality boxes, the LNER lounge, and Yorvik lounge available on matchdays, there is a huge opportunity to use these rooms to capacity to drive income as we have rarely sold out this season. We receive 17% income of gross food and drink sales from CGC from the hospitality and concessions in the stands, without the risk of holding stocks, trying to recruit staff etc.

It would be a lot of work to sum the total of unpaid bills that I have come across, however, I have raised approximately £113K through recovering debts, overpayments, and raising invoices relating to pre-takeover, so what we have recovered probably covers the unpaid bills.

The Ben Godfrey money was used to run the club and the remainder to settle the debts to Jason following the sale of Bootham Crescent.

As mentioned earlier the season ticket money was used to cover the close season and in my opinion the budget was overly ambitious so expenditure was higher than income. A lot of income, season ticket sales, merchandise, sponsorships arrives at the start of the season, whereas costs are more uniform throughout the year. When a club doesn’t have enough money to last the season its usual for the bite to come around the January/February timeline.

The Trust did receive an indication that no further funds would be made available, particularly as the budget prepared by the previous board forecast a small profit. However, it has since become clear that the budget was flawed, particularly as it didn’t account for the sale of different ticket types, complimentary tickets and various operational expenses. This resulted in an over-estimated ticket income of around 40% based on the 4,500 budgeted attendance. It is impossible to predict whether or not, or how, Jason would have provided additional funding, faced with such shortfalls.

The commercial function is one that the club must improve. The location of the club shop is not ideal and options to extend it into the office to make it bigger fell through as the cost was prohibitive when discussing with GLL. There is limited passing trade on matchday and the possibility of a pop up store on the grass approaching the South / East stand turnstiles have been discussed with Vangarde. Due to the fan zone getting very busy at times then adding a pop up stand has been refused within the fan zone. The merchandise website isn't user friendly, we would like to consolidate all the different websites into one, e.g. club, sponsorship, online shop, this will enhance user experience and make it easier for supporters to navigate around the site. The ticketing website has improved throughout the year, and we are working on more improvements for next season (e.g. hospitality tickets available directly on the ticketing website and introducing a process for purchase history determining big match ticket allocation).

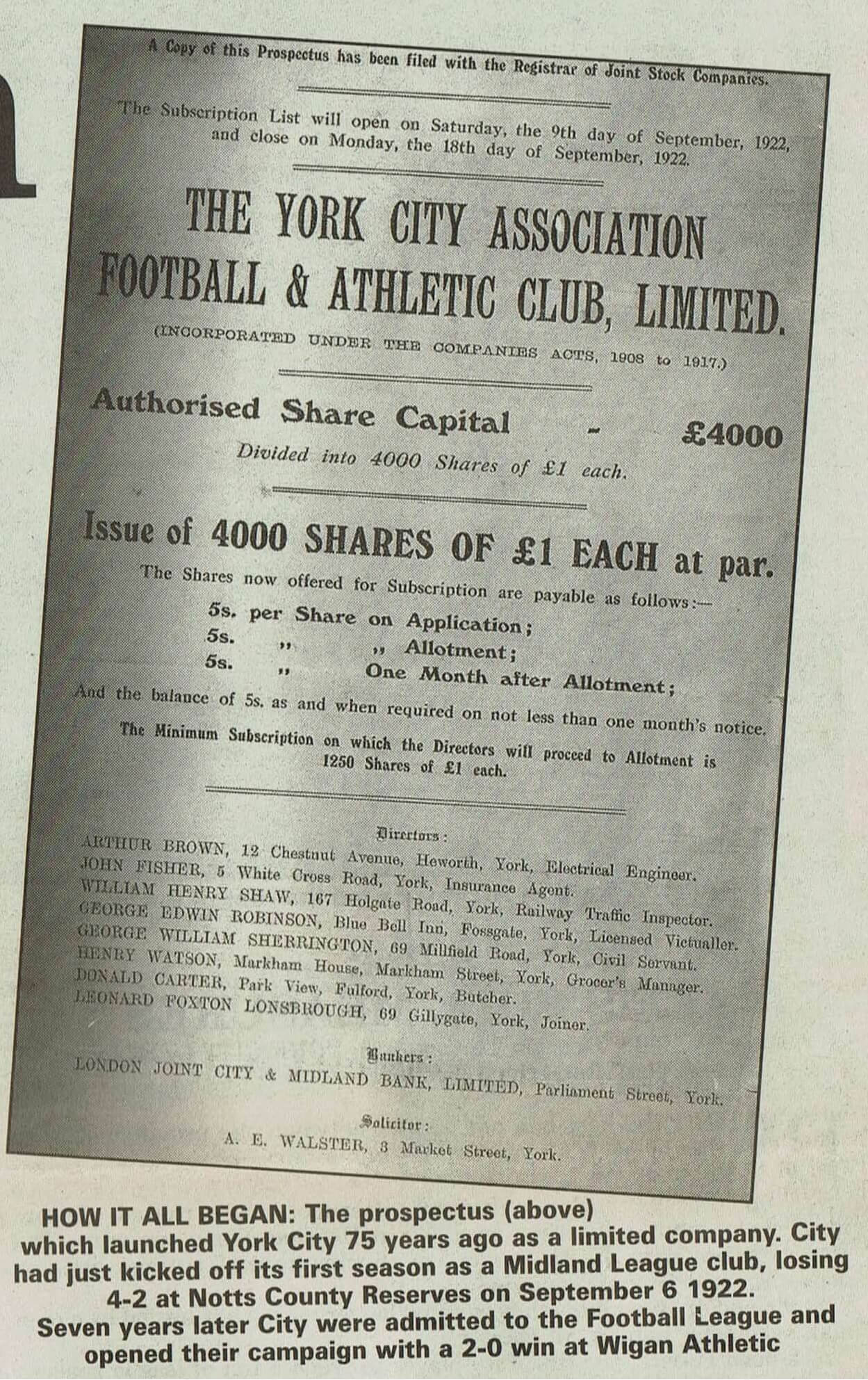

1922 - Want To Buy A Share?

See for accounts from earlier years and

20 years of accounts summarised plus profit / loss each year from 1922

")

")